What does “transferable points” mean?

Transferable points, also called “flexible points” are exactly that- moveable from one account (the bank) into another (the travel vendor)! Let’s dive in to what that means though!

There are four major credit card issuers in the USA, also called “big banks”- American Express, Capital One, Chase, and CitiBank. Each credit card issuer has one (or more) option of credit cards that accrue rewards points, most often based on spending. Often, these cards will be associated with large welcome bonus offers in points- an example is 60,000 points when you spend $4k in 3 months. Sometimes these cards will offer spending multipliers- 3x points per dollar spent on gasoline, for example. The cards will offer rewards points, not cash back or other incentives. There are very few cards on the market that offer both points and cash back- but I will cover one option later in this post!

What does the “transferable” part in the phrase “transferable points” entail?

Each credit issuer has a list of travel partners that they have contracts with. Each bank is different, although some vendors, such as Marriott and Air France, overlap with multiple card issuers. I have made a freebie which details where each bank transfers their points to, and you can grab that here!

While these points can be used in each bank’s portal to book various pieces of travel, they can also be transferred out to a travel partner and used to book hotels, flights, and more with that partnered vendor directly. This is actually where the best value is!

The price in the bank’s portal is often 1cent/1point for a booking, meaning a hotel room that is $300 per night will cost you 30,000 points in the bank’s portal, for example. But when the points are transferred out to book directly with the vendor, the booking value usually exceeds 2-3cents/point!

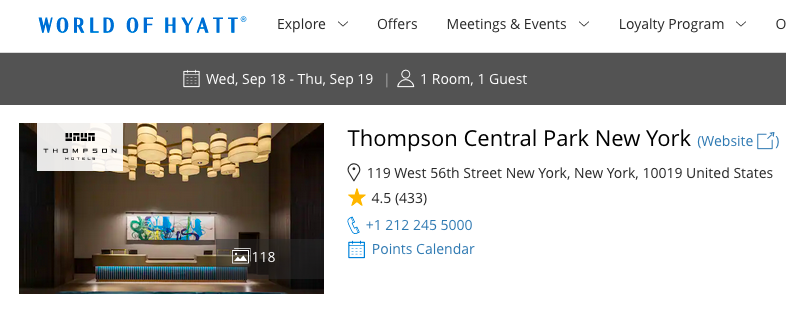

Let’s look at an example of booking a hotel through the bank’s portal versus directly with the vendor:

The Thompson Central Park Hyatt hotel in Manhattan, taken on the same Wed-Thursday night (one night stay, 9/18-19) in September 2024:

On Chase’s bank portal: rates are $1159 with taxes/fees, or 11590 points.

On Hyatt’s website: the same night is $1062, which is already cheaper. (That isn’t universally true, but is most often the case- that the vendor is cheaper than the bank’s portal for a cash rate.)

However, the same room can be booked directly on Hyatt’s for 29,000 WOH rewards points, for the same night. Those points can be transferred from Chase to Hyatt (and thus converted from Chase’s Ultimate Rewards points to World of Hyatt rewards points) at a 1:1 ratio.

This makes that same booking with a transfer an incredible value of 3.7cents/point! As you can see, your points go further in value when transferred directly to the vendor to make a booking. This is almost universally true.

Let’s look at another example, using a flight:

An Air France flight, Washington DC (IAD) to Paris (CDG) on a Monday in January 2025, nonstop, economy standard ticket (includes one carry on, no checked luggage, non-refundable fare):

Capital One Portal: $825, with a “price drop guarantee”, or 82500 points.

Air France website: $703, which, again, is already cheaper cash price directly from the vendor! Or, you could pay 20,000 points, plus $65 for taxes. Those same taxes are covered in the quoted $703 price.

So 70300/20000 equals a value of 3.5cents/point in value for this booking! But one would only get that value by transferring rewards points directly to the vendor (Air France in this case.)

So, how do I know I have an eligible transferable points card?

Only certain cards offered by each major bank has rewards points which can be accrued and transferred. Two questions to ask yourself in order to eliminate ineligible cards are: does this card accrue cash back rewards? And: does this card accrue points specific to one brand, also called a co-branded card? An example of this is an airline or hotel specific card. These cards are fine and can be advantageous for other reasons (free night/flight rewards, status perks), but they only accrue points with that one brand. For example, if you have an American Airlines card (through Barclay’s or Citibank), you are ONLY racking up AA miles! Those points can NOT be used for other airlines or hotels.

Here are the names of each bank’s transferable points cards:

Basically, if you have any of the following, you have a transferable points card already in your wallet!

American Express: Green, Gold, Platinum, or the business versions of each of these. AmEx calls their program Membership Rewards.

Capital One: VentureOne, Venture, or Venture X, or the business versions. They offer points through other cards advertised as cash back, such as the Spark/Spark business, but you’ll need one of the former three cards in order to transfer your points out of the bank. Capital One calls their program Rewards Miles.

Chase: Sapphire Preferred, Sapphire Reserve, or Ink Business Preferred. Chase also offers points through other cards advertised as having cash back rewards, such as their Freedom Unlimited, Freedom Flex, and Ink Business Cash. But you’ll need one of the first three cards in order to transfer your points out. Chase calls their program Ultimate Rewards.

CitiBank: Citi Strata Premier is currently the only transferable points card being offered, as of the time of this writing. If you still hold the Premier card or the Prestige card, you can still transfer your points out, but those cards are no longer being offered to new applicants. Citi also offers limited transfer point cards: the DoubleCash, Rewards+, and ThankYou Preferred cards transfer points, but only to the following partners: Choice Hotels, Wyndham Hotels, and JetBlue. So these last cards are probably not worth pursuing, in my opinion. CitiBank calls their program ThankYou points.

For most of these cards, you can receive a welcome bonus more than once. Chase and Capital One will let you receive a welcome bonus every 48 months. American Express has “lifetime” language, which means if you have received a welcome bonus already you are ineligible for another bonus on the same card (though rumor has it they will actually let you have another bonus after about 7 years.)

American Express also says you have to upgrade sequentially in order to be offered a welcome bonus on each, Green -> Gold -> Platinum. They won’t let you have the bonus if you downgrade, only if you upgrade, on these cards.

Both Cash Back and Points Options

Each of these banks will allow you to turn your rewards points into “cash back” in the form of a statement credit. This is always at a 1pt/1cent rate, (or less) and, as you can see from the above examples, is not nearly as good of a value as transferring those points out of the bank! Also, I would personally add, you’ve worked hard and spent a lot of money to accrue those points! So, in my humble opinion, cashing out your points is just a way of handing your hard earned money back to the bank. I would highly advise against cashing your points out! If you don’t have plans to travel immediately, leave them in the bank until you’re able to make plans.

Alternative offered through Capital One Venture Cards

Capital One Venture cards DO offer a kind of happy medium alternative between transferring points out, and redeeming them for cash back. CapOne offers the ability to redeem their points for any expense that codes as travel. This can be anything from train tickets, to parking, to transit, and can be a good value when redeemed for travel expenses that otherwise wouldn’t be able to be booked by transferring points out to a vendor.

One example, and a common way people use this benefit, is to buy tickets to Disney branded experiences- their theme parks, hotels, and cruises- through a third party vendor that codes as travel (because Disney as a company actually codes as “entertainment”).

This reduces the overall costs of the trip, and is also a way to make things financially feasible which someone wouldn’t otherwise be able to afford. (Still looking at you, Disney.) Unfortunately, the value is still only 1cent/1point.

So, I would highly advise to use this feature sparingly, and transfer your points out for a better value the vast majority of the time.

Why start with Transferable Points?

Transferable Points vs Co-Branded Cards

Co-branded cards are credit cards issued by the same banks as any other card, but are associated with only one other vendor, or brand. Basically, if the card says the name of a hotel or airline chain, it is a co-branded card.

The problem with co-branded cards is that they only accrue points with that one brand! There are times when this could be a good thing, such as earning status perks with that brand, or racking up points for a specific trip. However, especially when you are starting to bank points for travel, having flexibility is crucial.

There are two common scenarios that I can envision flexible points being much more valuable. One: a “cheaper” or better flight is available with a different airline than the co-branded card you were looking at, and two) you need to book with a different hotel chain- for various reasons.

Ultimately, it boils down to flexibility. Being able to be flexible- with vendors, dates, and to a certain extent, location- will save you money, time and probably strife as you are making reservations and traveling!

Reference Disclaimer:

All screenshots and quoted prices were accessed and accurate as of the date of publishing this post, May 18 2024.